Boss, let me tell you something that completely changed how I think about money. Last Diwali, I was helping my mother clean out the old steel almirah in my parents' home in Lucknow. You know how it is, na? Every Indian household has that one cupboard that hasn't been opened in decades, filled with old documents, faded photographs, and memories wrapped in yellowing paper.

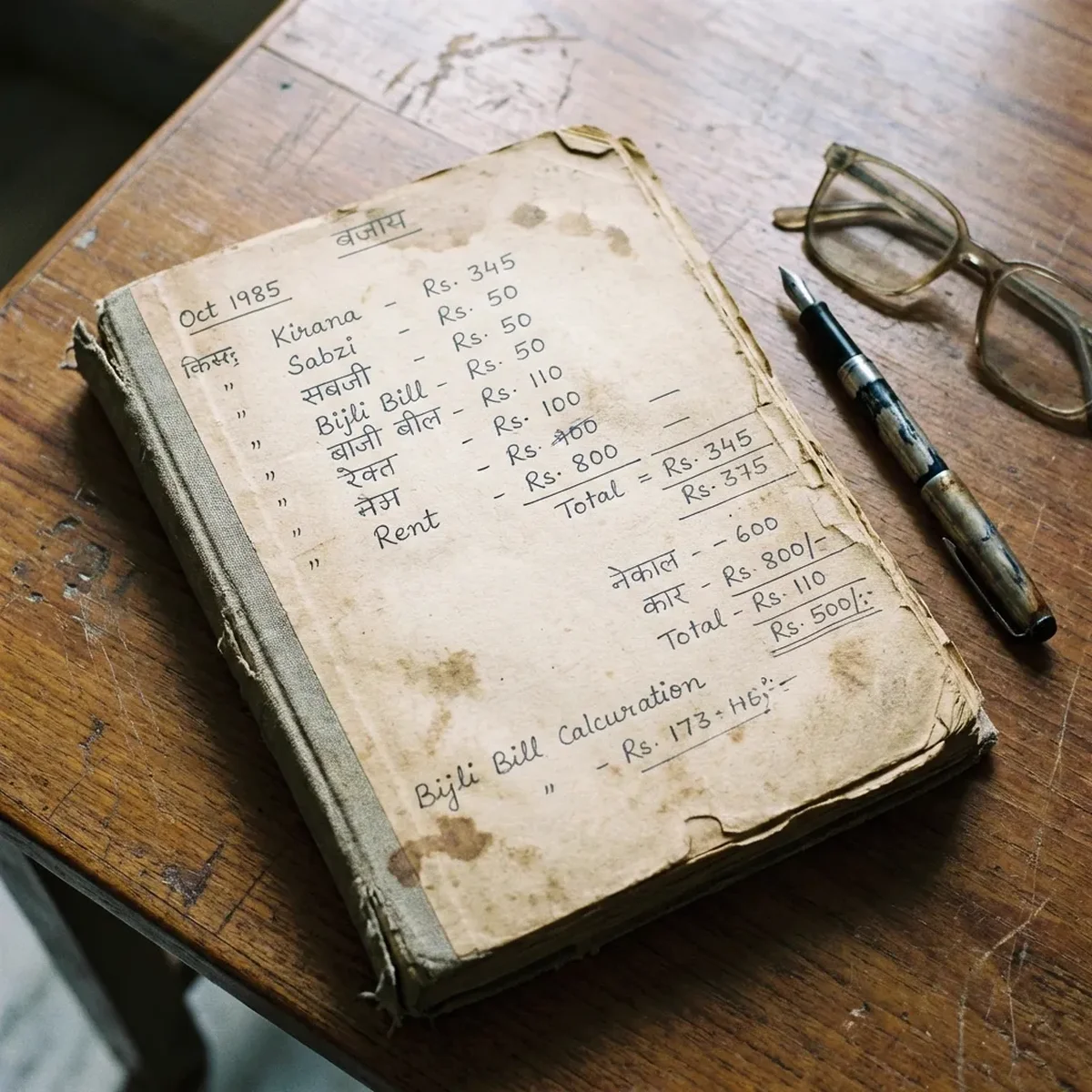

That's when I found it — a small, dog-eared notebook with a brown cover, held together with a rubber band that had lost all its elasticity years ago. On the first page, in my father's neat handwriting: "Household Budget - 1985."

Arre, I sat down right there on the floor, dust and all, and started reading. And let me tell you, within five minutes, I was practically in tears. Not from sadness — from the sheer disbelief at what things used to cost.

The October 1985 Entry That Broke My Brain

The first complete entry I saw was for October 1985. My father had meticulously recorded every expense for the month. Here's what I found:

| Item | 1985 Price | 2025 Price | Increase |

|---|---|---|---|

| Kirana (Monthly Groceries) | ₹345 | ₹8,500 | 24x |

| Sabzi (Vegetables) | ₹50 | ₹3,000 | 60x |

| Bijli Bill (Electricity) | ₹110 | ₹2,500 | 23x |

| Rent | ₹800 | ₹25,000 | 31x |

| Milk (Monthly) | ₹90 | ₹2,400 | 27x |

| Total Monthly | ₹1,395 | ₹41,400 | 30x |

Look at that table carefully, yaar. In 1985, my father was running an entire household — with a wife and two children — on less than ₹1,400 per month. And he wasn't poor. He was a government clerk, a respectable middle-class job. That ₹1,400 represented maybe 40-50% of his salary, which was around ₹3,000 per month.

Today, ₹1,400 won't even cover the vegetable expenses for a week in a metro city.

The ration shop - where every Indian household got their subsidized importants

The Ration Card Era: A System We've Almost Forgotten

One thing that struck me while reading my father's notes was how often he mentioned the ration shop. For those who don't remember or are too young to know, the Public Distribution System (PDS) was the backbone of Indian household economics in the 1970s, 80s, and 90s.

Every family had a ration card — usually a small, rectangular booklet with a distinctive color depending on your economic category. My family had a yellow card, which meant we were above the poverty line but still eligible for subsidized goods.

- Rice: ₹2 per kg (market price was ₹6)

- Wheat: ₹1.50 per kg (market price was ₹4)

- Sugar: ₹3 per kg (market price was ₹8)

- Kerosene: ₹2 per liter (important for cooking before LPG became common)

My father's diary shows that a significant portion of our monthly groceries came from the ration shop. He would go there on fixed days — usually the first and third Saturday of every month — and stand in line with hundreds of other people. Sometimes for hours. He wrote in one entry: "Ration shop line 3 hours. Got 10kg wheat, 5kg rice. Sugar not available."

Can you imagine waiting three hours to buy basic groceries? But that was the reality. And honestly, for all its inefficiencies, the ration system kept millions of families fed at prices they could afford.

A typical middle-class kitchen of the 1980s - simple, functional, and frugal

The Kitchen Economics of the 1980s

Looking at my father's detailed notes, I realized something important about how Indian households functioned in those days. The kitchen was the center of all financial planning. My mother — like most Indian women of that era — was importantly a financial manager who never got a degree but could stretch a rupee further than any MBA could dream of.

Here's how the monthly grocery budget of ₹345 was typically broken down:

- Dal (various types): ₹60 (about 5 kg at ₹12/kg)

- Cooking oil: ₹80 (about 4 liters at ₹20/liter)

- Atta (wheat flour): ₹40 (about 10 kg at ₹4/kg)

- Rice: ₹30 (about 5 kg at ₹6/kg)

- Sugar: ₹25 (about 3 kg at ₹8/kg)

- Spices and masala: ₹50

- Tea and milk powder: ₹30

- Miscellaneous: ₹30

What's remarkable is how little variety there was. No fancy breakfast cereals, no imported cheese, no "health foods" or "organic options." The diet was simple — roti, dal, sabzi, rice, and occasional non-veg on Sundays (for families that ate it). And yet, people were generally healthier. No obesity epidemic, fewer lifestyle diseases.

My mother tells me she used to make pickles, papads, and even masalas at home. Not as a hobby, but because buying readymade stuff was considered wasteful. "Paisa ka value tha tab," she says. There was value in money then.

The doodhwala - a familiar morning visitor in every Indian colony

The Doodhwala and the Economics of Trust

One of the most fascinating entries in my father's diary was about milk. He had written: "Milk - ₹3 per liter. Sharma ji doodhwala. Payment monthly."

₹3 per liter. Today, Amul Full Cream milk costs ₹66 per liter. That's roughly a 22x increase in 40 years, maybe more depending on which variant you buy.

But here's what's more interesting — the system. There was no Amul packet delivery app, no BigBasket subscription. There was Sharma ji (or whatever the local milkman's name was in your area). He had a bicycle with large metal cans attached to either side. He would come every morning at 6 AM, sharp—or at least that was the plan, though honestly some days he'd show up closer to 6:30. You'd hand him your steel container, he'd fill it with fresh buffalo milk, and move on to the next house.

Payment was always at the end of the month. No advance, no security deposit. Just trust. He knew every family in the colony. He knew who had how many members, who needed more milk in winter (for making chai and hot drinks), who had just had a baby and needed extra. I think that level of personal connection is something we've completely lost now.

This was the informal economy at its best. No GST, no invoices, no digital payments. Just relationships built over years.

The Vegetable Vendor: Inflation's Most Visible Victim

The neighborhood sabzi wala - still surviving, barely

If there's one category where inflation has been absolutely brutal, it's vegetables. My father's ₹50 monthly vegetable budget in 1985 has become ₹3,000 or more today—probably closer to ₹4,000 in some metros. That's roughly a 60x increase, maybe higher — double the average inflation rate, from what I've seen.

Let me give you some specific examples:

| Vegetable | 1985 (per kg) | 2025 (per kg) |

|---|---|---|

| Tomato | ₹1.50 | ₹40-80 |

| Potato | ₹1 | ₹25-40 |

| Onion | ₹2 | ₹30-60 |

| Cauliflower | ₹3 | ₹50-80 |

Remember the tomato crisis of 2023 when prices hit ₹200 per kg in some cities? My father laughed and said, "Beta, tomato ₹200 ka? Humare zamane mein pura hafte ka sabzi ₹10 mein aa jata tha."

And he wasn't exaggerating. His diary confirms it.

The Storage Economy: How We Preserved Wealth

The traditional Indian pantry - buying in bulk was survival strategy

One thing you'll notice if you ever visit an older Indian home is the amount of storage. Large steel containers (dibba or dabba), gunny bags of rice and wheat, jars of pickles and preserves. This wasn't just tradition — it was economic strategy.

My father's diary has entries like: "Bought 50 kg wheat at ₹3.5/kg. Next month expected price ₹4." He was importantly hedging against inflation by buying in bulk when prices were low. Not sure if he thought of it that way at the time, but that's effectively what it was.

This practice — which we might call "inventory management" in corporate speak — was taught to every Indian housewife by her mother. Buy atta and rice in bulk after harvest season when prices are low. Make summer pickles to last through winter. Dry mangoes and vegetables when they're cheap and abundant. My grandmother had probably 15-20 large jars in her kitchen at any given time, each preserving something different.

This wisdom is slowly being lost. With Amazon Fresh and instant delivery, we've stopped thinking about seasonal availability. We expect tomatoes in December at the same price as June. And when that doesn't happen, we complain about inflation. Seems like we've traded convenience for financial common sense.

The Big Shift: From Kirana to Supermarket

The modern shopping experience - convenient, but is it cheaper?

My father shopped exclusively at the neighborhood kirana store. The owner, Pandey ji, knew our family for three generations. He gave us credit when money was tight. He would recommend which dal was fresh this week. He remembered that my mother preferred the smaller elachi brand over the larger one.

Today, I shop at a supermarket. It's air-conditioned. The shelves are organized. I can compare prices of 15 biscuit brands at once. There's a rewards program that gives me 2% back. It's objectively more "efficient."

But here's what I've realized: the supermarket has made me buy more, not less. Those "combo offers" and "buy 2 get 1 free" deals? They're designed to make you purchase things you didn't plan to buy. The 2% reward I earn? I probably spend 20% extra on impulse purchases just walking through those aisles.

Pandey ji never offered 2% rewards. But he also never made me buy a ₹200 jar of "artisanal" pasta sauce that I used once and forgot in the fridge.

What My Father's Diary Teaches About Inflation

After spending hours with that diary, here are the lessons I've taken away:

Lesson 1: Inflation Hits Different for Different Things

Not all prices rise equally. Vegetables (60x) have increased much more than electricity (23x) or even rent (31x). This is called "relative price inflation," and it matters because different families spend differently. A vegetarian family gets hit harder by vegetable price rises. A family in a rented home suffers more from rental inflation.

Lesson 2: Credit and Trust Can Beat Inflation

My father's diary shows he often bought things on credit — from the kirana store, the doodhwala, even the vegetable vendor. This wasn't debt in the modern sense. It was a community-based system of trust that allowed families to manage cash flow without paying interest. We've replaced this with credit cards that charge 40% APR.

Lesson 3: Self-Sufficiency Was Anti-Inflation

Making pickles, papads, and masalas at home wasn't just about taste or tradition. It was protection against price volatility. When mango prices spiked, our homemade pickle was already in the jar. When masala prices rose, we had last year's batch. Modern convenience has made us vulnerable.

Lesson 4: Salary Growth Hasn't Matched Lifestyle Inflation

My father's salary in 1985 was ₹3,000. Today's equivalent government clerk earns about ₹35,000-40,000. That's roughly 12x increase. But household expenses have increased 30x. The gap is filled by: working spouses, smaller families, debt, and reduced savings. We're not getting richer — we're running faster just to stay in place.

The Emotional Weight of These Numbers

I need to be honest with you, yaar. Reading my father's diary wasn't just an economic education. It was emotional.

I saw his handwriting change over the years — confident and neat in the early pages, slightly shakier in later years. I saw entries about my school fees increasing every year. I saw notes about borrowing money from his brother for my sister's wedding. I saw calculations where he was clearly worried about making ends meet. Honestly, it was hard to read some of those pages without feeling a lump in my throat.

And yet, he never let us feel it. We always had food on the table, clothes on our back, books for school. We never knew he was sometimes operating on a margin of maybe ₹50-100 per month. I think that's what parents from that generation did—they carried all that weight silently.

This is the story of millions of Indian middle-class families. Our parents absorbed the stress of inflation so we didn't have to feel it. They cut their own expenses — new clothes for themselves, entertainment, personal indulgences — so our lives could be normal.

What This Means for Your Financial Planning

Before I get too sentimental, let me bring this back to practical advice:

- Track your expenses like my father did: Not with apps that auto-categorize and make it too easy to ignore. With intention and detail. Know where your money goes.

- Build a buffer: Aim to have at least 6 months of expenses saved. Inflation is relentless, but having savings gives you options.

- Invest in assets that beat inflation: My father's salary couldn't keep up with inflation. But if he had invested in property or gold, those assets would have kept pace or exceeded it.

- Develop skills, not just degrees: The best hedge against inflation is earning power. Skills that remain valuable as economies change.

- Build community relationships: In a crisis, your network might save you more than your networth. The kirana shop owner who gives credit, the neighbor who shares excess vegetables, the friend who offers a temporary loan without interest.

Use our Inflation Calculator to compare purchasing power across decades.

Final Thoughts: The Diary Closes, The Lessons Remain

I've put my father's diary back in the almirah, but in a better spot — where I can find it again. I've also started my own expense journal. Not a spreadsheet on Google Sheets, but an actual notebook. There's something about handwriting that makes you think more carefully about what you're recording.

My father is 73 now. When I showed him this article, he laughed at some memories, got quiet at others. At the end, he said something that stuck with me: "Beta, numbers change, but the struggle remains the same. Rich or poor, we're all just trying to give our families a better life than we had. That was true in 1985, it's true today, and it'll be true in 2065."

He's right, of course. He usually is.

What I've realized — and I think this is probably the most useful thing I've taken from this whole exercise — is that tracking your own expenses with this level of detail gives you a kind of clarity that no budgeting app can match. When you see the numbers over years, patterns emerge. You notice where your money quietly leaked. You see which costs grew faster than you thought. Maybe your grocery bill went up 8% but your eating-out spend jumped 25%. That kind of insight doesn't come from glancing at a UPI statement.

The numbers in that diary are from a different era. But the feelings — the anxiety about rising prices, the pride in providing for a family, the hope that the next generation will have it better — those are timeless.

And if you ever find your parents' old household records, take the time to read them. It's not just economic history. It's family history. It's your history.